India’s commercial real estate market is experiencing a remarkable period. In 2024, India’s office market reached a historic peak in net absorption of nearly 49.56 million sq. ft., while gross leasing volumes reached an unprecedented 89 million sq. ft. across the top eight cities, figures that would have seemed improbable in the depths of the pandemic. By the first nine months of 2025, the momentum had not slowed: India’s gross leasing volumes reached 56.5 million sq. ft., up 5.7% year-on-year, and net absorption for Jan–Sep 2025 reached a record 40 million sq. ft.

At the heart of this surge is a structural force that AV systems integrators cannot afford to ignore:the rise of Global Capability Centres. In 2024, GCCs accounted for 37% of overall office leasing in India. CBRE projects that GCCs will account for 35–40% of total office space absorption in 2025. They have also recorded their best-ever nine-month performance in 2025, having leased 20 million sq. ft. so far.

These are not passive tenants occupying generic office floors. They are transforming the very nature of how workspace is conceived, delivered, and operated in India, and, in doing so, are fundamentally redrawing the opportunity map for the AV systems integration industry. For AV systems integrators and consultants, this transformation is not background noise. It is the signal that should be reshaping every conversation about strategy, partnerships, and positioning.

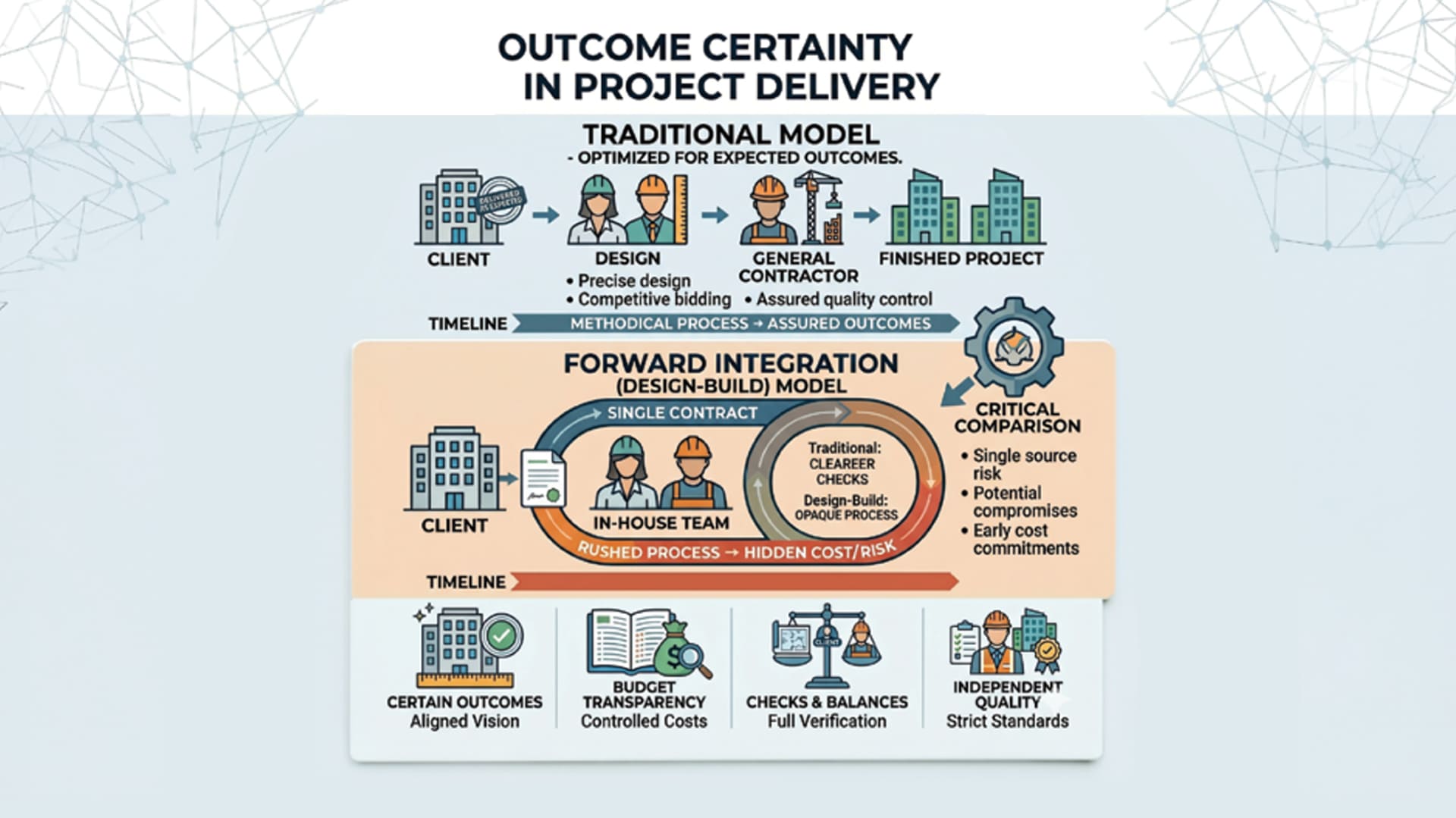

The forward integration shift

Before COVID, the dominant model in Indian commercial real estate was straightforward: a developer delivered a warm or bare shell, and

an interior designer, alongside a PMC (project management consultant), would design (with AV consultants working either directly with the

client or with the architect to provide the AV part of the scope). A fit-out contractor would then come in, followed by the tenant’s IT and AV vendors. Each party had a defined lane. The AV integrator typically arrived at the tail end of a project, worked to a specification handed down by a consultant or the client’s IT team, installed, commissioned, and left.

That world is receding rapidly. Flexible managed workspaces now behave less like properties and more like operating systems, offering plug-and play facilities, infrastructure, compliance, talent access, and innovation ecosystems. Real estate developers and managed workspace operators have moved up the value chain, integrating what were once separate scopes of fit-out contractors, IT integrators, and AV specialists into bundled “GCC-as-a-Service” offerings.

AV optics

If this shift is disorienting for AV systems integrators, it is existential in a different way for AV consultants and designers. The traditional consulting model is built on an independence premium; the consultant’s value lies in serving as the occupier’s trusted advisor, translating business requirements into technology specifications, and holding integrators accountable to those specifications. That model assumes direct, sustained engagement with the end-user throughout design, tender, and delivery.

Forward integration compresses precisely that space. When a managed workspace operator or a GCC-as-a-Service platform pre-selects AV technology categories, standardises room configurations, and awards preferred-vendor arrangements, the consultant’s independent specification role is either absorbed into the operator’s in-house team or reduced to a compliance-checking exercise. Consultants increasingly find themselves working through a channel, namely the operator, the developer, or the fit-out contractor, rather than directly with the occupier. Scope dilutes. Fee structures compress. And the hard-won client relationship that consulting practices depend on for repeat work migrates to the platform.

In the AV industry, the rise of managed flex space is a double-edged development. On the one hand, it represents an extraordinary volume. On the other hand, it structurally compresses how and where AVSI companies operate.

When a Smartworks or an Indiqube pre-deploys AV infrastructure across hundreds of meeting rooms as part of their standard managed product, the integrator’s engagement shifts from a one-to-one client relationship to a platform-supply relationship. The decision about which AV technology is deployed and by whom moves from the occupier to the operator. The transaction becomes a volume contract with the flex provider, not a consultative engagement with the end-user.

I have seen this shift first-hand. Projects that would have historically involved a three-month consultative cycle with a GCC’s real estate and IT teams are now being resolved in days through the managed workspace operator’s pre-approved vendor list. The AV conversation happens before the occupier even signs the lease.

Here is the other side of that signal. As GCCs shift from cost centres to innovation hubs, the AV scope within these facilities has expanded dramatically. These are not environments served by commodity AV. They require immersive collaboration rooms, advanced videoconferencing aligned with global UC standards, broadcast-grade allhands spaces, experience centres for client and leadership visits, and increasingly, integrated room analytics and IoT-driven utilisation dashboards. The integrator who positions themselves as a technology consultant, not a box-and-cable vendor, wins this work.

New GCC entrants are leveraging flexible spaces to enable rapid, agile expansion, while established companies are setting up large, dedicated campuses in major Indian cities. That bifurcation matters for AVSI’s go-to-market: the two segments require very different engagement models.

Broadly, there are two strategic moves our AV partners can consider:

Integrate upstream: The integrator who waits to be called in at the fit-out stage will increasingly find the scope already committed. The strategic move is to establish formal partnerships with managed workspace operators, flex providers, and GCC-as-a-Service platforms, becoming their preferred AV technology partner embedded in the product specification. This means standardising your offering, accepting framework pricing, and competing on quality of delivery and support, not on project margin alone.

Build a managed services spine: GCCs are increasingly leaning towards long-term managed workspace agreements and customised solutions.

The same preference applies to AV. A GCC that has standardised on a particular video collaboration ecosystem wants one throat to choke for support, firmware updates, room analytics, and lifecycle management. AVSI companies that can offer an AMC-plus-managed-service wrapper with SLAs and a helpdesk retain the relationship beyond commissioning. Those that cannot will be commoditised.

In the near term (12–24 months), expect the volume of GCC fit-outs to remain strong, with the primary battleground being mid-market GCCs

(100–500 seats) choosing between managed flex and dedicated leased space. AV integrators should be actively working both channels. In the medium term (3–5 years), GCCs are projected to account for nearly half of all enterprise flex seat uptake, and the AV technology embedded in that supply chain will largely be determined by decisions made today. The long-term story, driven by AI workloads, R&D mandates, and India’s deepening role as a global innovation hub, points to increasingly sophisticated AV environments and to clients who understand the ROI of getting that environment right.

The building has become the brief. The question for every AV systems integrator in India is whether they are in the room when that brief is written or arriving after it has already been decided.

About Author

Swapna K L is a Senior Principal Consultant at 3CDN Workplace Tech Pvt. Ltd., a leading workplace technology design and consulting firm specialising in AV, ICT, Smart Building, and Acoustics. She carries over 12 years of experience in the AV / Multimedia industry, while delivering large projects for clients such as SAP, Wells Fargo, Morgan Stanley to name a few.